If you’re shopping for a used vehicle, there’s more to consider than just make, model, and price. For most buyers, securing financing is a key part of the process, and that usually starts with your credit score.

So, what credit score do you need to get approved for a used car loan in Canada? In this guide, we’ll break down what qualifies as a good score, how it affects your financing options, and how you can still get approved even if your credit isn’t perfect.

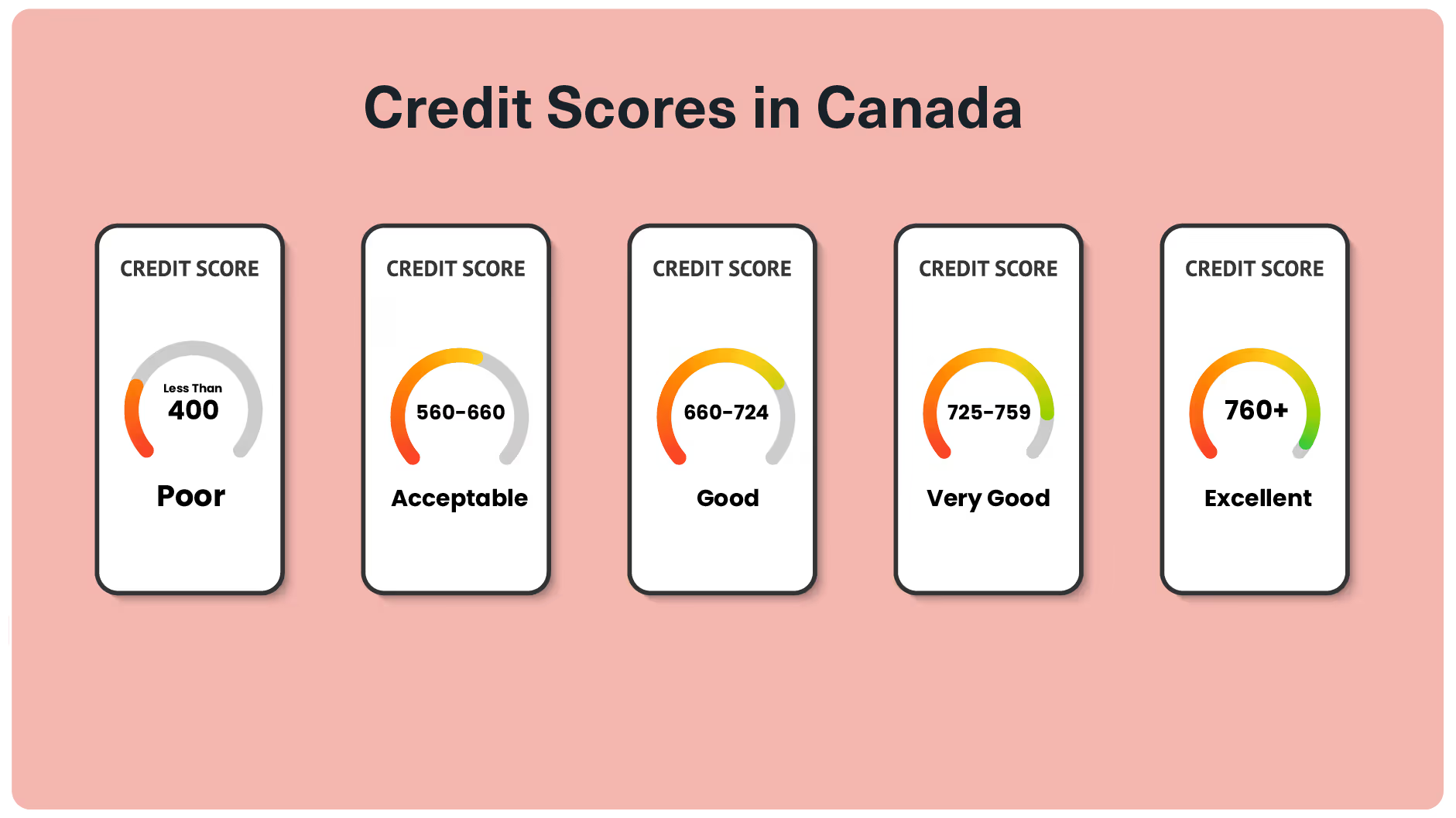

What Credit Score Do You Need to Finance a Used Car?

If you’re applying for a used car loan, a credit score between 650 and 750 is generally considered good. While lenders also look at income, debt levels, and payment history, this range typically signals strong credit health—no recent missed payments, collections, or high balances on credit cards.

With a score in this range, you’ll likely qualify for competitive interest rates and flexible loan terms. The higher your score, the more attractive your financing options become, including access to lower rates and longer repayment periods.

Clutch Works With All Types of Credit

While a strong credit score can help you qualify for the best possible rates, it’s not the only factor lenders consider. At Clutch, we look at the full picture, including your credit history length, credit utilization, and debt-to-income ratio. That means even if your credit isn’t perfect, you may still have options.

Whether you’ve had late or missed payments, collections, or other credit challenges, we partner with lenders who specialize in helping borrowers with less-than-ideal credit. You could still qualify for a competitive auto loan, even if other lenders have rejected your loan application.

You can fill out our quick online application to see your financing options with no credit impact.

What Factors Influence Your Credit Score?

Your credit score is a key indicator of how reliably you manage your debt. It’s calculated using information from your credit report, which is maintained by major credit bureaus like Equifax, TransUnion, and Experian.

While there are different scoring systems, most lenders in Canada rely on the FICO model. This model generates a score between 300 and 900, with higher scores giving you access to better loan terms and financial products.

Your FICO score is based on five key factors, each carrying a different weight. Here’s how they break down and how you can improve each:

Payment History (35%)

This is the single most important factor. It tracks whether you’ve consistently made on-time payments on credit cards, loans, lines of credit, and other debt. Missed or late payments, as well as accounts sent to collections, can significantly hurt your score.

To keep this part of your score strong, make at least the minimum payment on all your accounts by the due date. If you have old unpaid debts, resolving them—either by paying in full or negotiating a settlement—can also help rebuild your credit.

Amounts Owed (30%)

This factor looks at how much debt you currently carry. It includes total outstanding balances, the number of accounts with debt, how much is owed on installment loans, and—most importantly—your credit utilization ratio. That ratio compares your credit card and line of credit balances to your available limits.

A high credit utilization ratio can bring your score down, even if you make payments on time. To help boost this part of your score, aim to keep your balances well below your credit limits—ideally under 30%.

Length of Credit History (15%)

This part of your score reflects how long you’ve been using credit. It looks at the age of your oldest account, the average age of all your accounts, and how recently you’ve used different types of credit.

A longer credit history shows lenders you’re experienced with managing debt. While you can’t fast-track time, you can preserve your score by keeping older accounts open and avoiding unnecessary new ones.

New Credit (10%)

New credit activity plays a small but meaningful role in your FICO score. This category tracks:

- How many new accounts you’ve opened

- The time since your most recent account was opened

- The number of hard credit inquiries in the last 12 months

- How recently has a lender performed a hard check

Opening several new accounts in a short time can signal financial distress and may hurt your score. To protect this part of your credit profile, avoid applying for multiple new accounts unless necessary.

Credit Mix (10%)

This category looks at the variety of credit types you manage. A healthy mix might include revolving credit (like credit cards) and installment loans (like car loans, mortgages, or student loans).

Lenders like to see that you can handle different types of debt responsibly. While diversifying your credit types can help, avoid opening new accounts just for variety—it can hurt your score in the short term by lowering your average account age and increasing hard inquiries.

You Can Check Your Own Credit

Keeping tabs on your credit is a smart habit, especially if you’re planning to finance a car. Regular credit monitoring lets you track your progress, catch errors or suspicious activity early, and see how your financial decisions are impacting your score over time.

You can check your credit report and score for free through services like Credit Karma, Borrowell, or directly from credit bureaus like Equifax or TransUnion. These tools provide insight into where you stand and help you take informed steps to improve your credit.

Fair Financing and Quality Cars With Clutch

Finding a reliable vehicle and getting approved for financing shouldn’t be mutually exclusive. At Clutch, we make both possible. Every car on our site has passed a 210-point inspection, comes with a 3-month or 6,000-km warranty, and includes a 10-day or 750-km money-back guarantee for peace of mind.

We also offer financing options for all types of credit. Whether your score is strong or still a work in progress, you can apply online in minutes and see your loan options, without affecting your credit. Before you apply, try our car loan calculator to get an idea of your potential monthly payments and find a budget that works for you.

Best of all, the entire experience is 100% online. Choose your car, get pre-qualified, and schedule delivery right to your door. If you have a trade-in, we’ll handle that too. Ready to get started? Browse our inventory today.

FAQs About Credit Score for Financing a Used Car

What credit score do I need to finance a used car in Canada?

While requirements vary by lender, a score of 650 or higher is generally considered good for financing a used car. With scores above 720, you may qualify for the best rates and terms.

Can I get a car loan with bad credit?

Yes, it’s possible to get approved with a credit score below 600, especially if you work with lenders who specialize in bad credit financing. Keep in mind, interest rates will likely be higher, and you may need a larger down payment.

Does checking my own credit score lower it?

No. Checking your own credit is considered a soft inquiry and does not affect your score. Only hard inquiries—when a lender checks your credit for a loan application—can cause a small dip.

How can I improve my credit score before applying for a car loan?

Pay bills on time, keep credit card balances low, avoid opening new accounts unnecessarily, and check your credit report for errors. These steps can help raise your score over time.

Which credit score model do car lenders use?

Most auto lenders in Canada use versions of the FICO score, though some may use other models. Your score can vary slightly depending on the credit bureau and scoring system used.

Is no credit the same as bad credit when applying for a car loan?

Not quite. While both can make it harder to get approved, lenders may view no credit history more favourably than a history of missed payments or defaults.

.avif)

.avif)

.avif)

-02.png)

_Thumbnail.avif)